If you’re engaged in the pursuit of happiness, it’s important to recognize that there are many aspects of happiness. In a previous post about happiness, we divided those aspects into seven areas: personal growth, spirituality, health, family, social, career, and finances.

Today, I want to explore how and why a healthy financial life affects personal happiness and how to determine how much is enough.

Money can’t buy happiness. But money can buy ease, mobility, and access to things that greatly affect your well-being, such as medical attention and a healthy lifestyle.

Being happy with your finances isn’t about having the perfect amount of money. There are low-income households full of happiness, and there are high-income households rife with unhappiness.

Financial happiness isn’t about attaining a certain dollar amount. It’s about sparing yourself the stress and strain of living under an inappropriate financial structure.

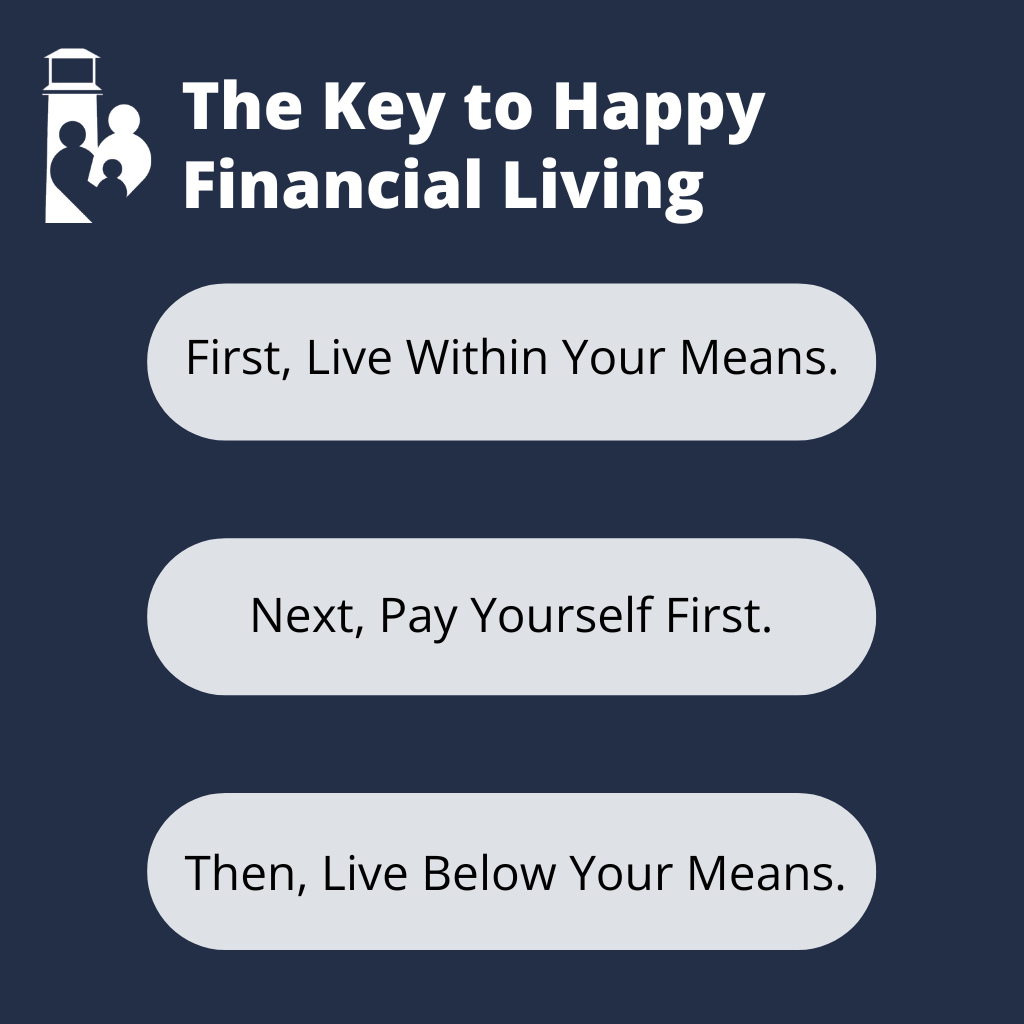

Key to Happy Financial Living

The key to financial happiness can be summarized by this essential advice: do not spend more than you make.

This seems like a simple answer (and it is!), but simple doesn’t always mean easy. Financial realities vary; the trick is to be happy with what you can do in your given reality.

Let’s break this down into three parts:

First, Live Within Your Means. Advertising encourages us to buy, buy, buy! But so many joy-bringing activities don’t cost a dime. A walk in the woods can be relaxing and enjoyable, and it’s totally free. If you need a vacation but don’t have a huge budget, consider a camping trip versus a two-week European extravaganza.

Next, Pay Yourself First. When we work from our 20s through our 60s (and beyond!), it’s important to place our money into different buckets. One simple and powerful tactic is to pay yourself first, meaning to put money into a savings account or retirement fund each time you’re paid.

Ideally, that’s a habit to begin as soon as we become gainfully employed. You have kids of your own, do them a favor and teach them how to save at a young age. At age 50 or 60, pondering what to do about an unresolved financial future is a lot more challenging.

Say you’ve financed a car and made the last payment. Many people will sell the paid-off car and finance a new car. Instead of that, pay yourself first. Keep driving the paid-off car. Each month, continually “pay yourself” your former car payment. When you need a new car, you’ll be able to pay cash for it — a wonderful feeling.

Pay yourself, not the finance company.

Then, Live Below Your Means. Financial troubles, usually because of spending, are the number one cause of marital conflicts. Sometimes, people get into trouble in their 30s and 40s as their financial means increase. If they match that increase with a lifestyle upgrade, there’s no substantial gain.

If your lifestyle remains the same and your finances increase, you have the opportunity to be more deliberate with your money. You can put away for the future, build a retirement account, save for higher education, a new car, and most of all, prepare for life’s unexpected crises.

How Financial Wellness Works

But why am I, a physician, talking to you about this?

Because financial health has a real, measurable effect on human health. Here’s what enough money can buy us and what a dearth of money costs us:

Proper health care. Most medical dollars are spent treating acute medical diseases. Treating a medical crisis is expensive. It costs us financially, physically, socially, and mentally. Not being able to afford care — including affording to properly heal before returning to work — hurts your health.

Access to proper health care also helps you access early detection and/or prevention. This is life-saving and cheaper than treating a disease once it’s developed. Having the money to spend on preventive services is a huge boon. You need to be able to afford to take care of yourself.

Stress and strain. Some stress is unavoidable. But there are stressors we can minimize and even eliminate. When finances become an obstacle to proper stress elimination — or worse, when they cause stress — you have a problem.

Chronic stress reduces both quality of life and lifespan, and financial problems generate copious and compounding stress. Ample resources and a plan for our financial future lower the risk of being hurt by factors we can’t control. That way, when something unpleasant and unexpected comes, we’re better equipped to handle it independently.

Food selection. While they may be less expensive upfront, chronically consuming processed foods — foods loaded with carbs and unhealthy preservatives — takes a tremendous toll on the body, leading to many expensive illnesses. Repairing the damage from that eating style is the high cost of cheap food.

If, on the other hand, we spend money on healthy, organic food, the benefits are long-term, and the amount of future financial strain is significantly smaller. (See my blog post on grocery shopping for helpful tips!)

Conclusion

Financial well-being is a significant part of a happy, healthy, fulfilling life.

Whether you consult with a financial planner or watch videos online, it pays to become financially literate. Getting into the habit of responsible financing gives you security, whatever your financial means. I’ve met people who make close to minimum wage who retired at 65 with plenty in the bank.

Never having to scramble for money imparts peace of mind. And peace of mind is happiness.